The Smart Systems and Flexibility Plan is the UK government’s and Ofgem’s proposal to achieve Net Zero emissions in the energy system. Most of the other current BEIS consultations are detailed looks into elements of this plan. Our response is long and detailed, including pointers as to how to reform and improve the plan and the system to be affordable, reliable and resilient, and is available on a consultancy basis. This is one section of our response.

Where We Are Now

Achievements in decarbonisation and procuring flexibility on both transmission and distribution grids have been laudable. However, the grid and entire system appear to be both rickety and deteriorating inexorably, as indicated by (for example) the:

- Number of grid failures and near-misses;

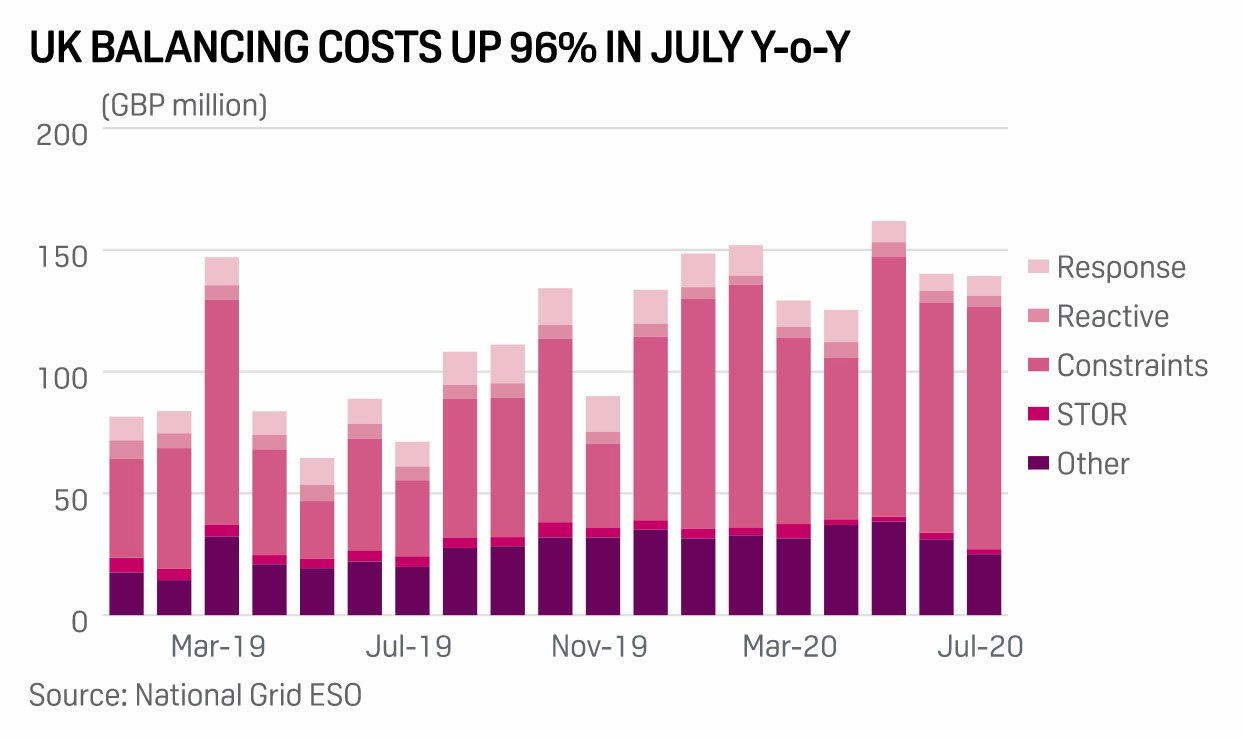

- Ever-escalating (currently £1.5bn p.a., or 15% of all energy expenditure, p52) costs of balancing and flexibility services;

- Ever-increasing frequency, types and scale of interventions;

- Continually aging grid and grid-connected assets;

- The cost of £1-1.25bn capital plus ~£125m annually to connect each GW of new offshore wind (see below), and

- Anticipated ever-increasing nature of all of these.

It is evident that much needs to change, to fit the grid and entire system for a Net Zero world. We cannot deliver 21st-century needs with a system (including, most importantly, its regulation and contracting) designed for the 20th century plus numerous patches. Indeed, these patches are so numerous that it is increasingly difficult to discern the system underneath that is being patched, which is why electricity costs make up less than half (and decreasing) of electricity prices, and the British electricity system is one of Europe’s most expensive and getting continually dearer.

The savings trumpeted as successes for each patch can be likened to the receding of a wave on an in-coming tide: it does nothing to reverse the rising sea level. The main difference is that, on present policies and proposals, the tide will never turn.

The focus on DSR, V2G and distributed systems to support the grid is analogous to having a flat car battery, and connecting mobile phones to its USB sockets to try to start the engine. (In fact, the differences in scale are orders of magnitude worse than this.) They don’t have the scale, duration or ability to take the loads.

You Get What You Pay For

Reforming markets to reward flexibility, stability and other services is right and necessary, but only a very tentative start of addressing what is needed. You get what you pay for, so if you pay for only part of what you need, you get only part; if you pay for the wrong things, you get the wrong things.

Current energy markets pay for:

- Energy;

- Capacity for future energy;

- Ancillary services;

- Some measures of flexibility;

- Minimising short-term costs;

- Quick fixes, as opposed to optimal solutions.

The markets do not pay for:

- Delivering the energy when needed;

- Emissions reduction;

- Stability;

- Duration;

- Back-up for longer periods of need;

- Minimising medium- and long-term costs;

- Designing and optimising the system in the medium and (especially) long terms;

- Minimising whole-system costs: construction, operation, maintenance and control;

- Minimising whole-system contractual costs to provide the required services;

- Minimising the costs, instabilities and disruption of the energy transition;

- Major new capital investment (other than a few market-distorting special arrangements such as CfDs and OFTOs);

- Enabling the best solutions to be built (e.g. lead time, breadth of capabilities, whole-system cost-effectiveness);

- Optimisation of offshore and onshore systems and assets;

- Introduction of new technologies.

Therefore, in order to obtain what the markets do not pay for, special market-distorting interventions and contracts are needed, adding enormously to grid costs while reducing flexibility, controllability, stability and resilience. As the Soviet Union discovered before it collapsed, this kind of central planning does not work in the medium and longer terms.

Excessive Costs of the Current System

National Grid’s (NG’s) Network Options Analysis 2021 proposed ~£16bn grid reinforcement to accommodate ~17GW new offshore wind by 2025, almost £1bn/GW. This ignored that NG would also have to source balancing and stability services elsewhere, and connect those services, and manage the complexities and the disturbances between the source of the problem (the wind farms’ grid connections) and the solution (the balancing and stability service providers’ grid connections); Storelectric guesstimates the total cost to be of the order of £1.25m/GW capital costs alone. Based on previous reports, annual maintenance costs are ~5% of that, and management costs are also ~5%, so (even before considering the costs of the balancing and stability contracts) annual costs are of the order of ~£125k/GW.

Non-grid solutions to this have potential to provide enormous savings (well over 50%) on this, saving the majority of the grid costs of the energy transition. BEIS, Ofgem and National Grid are right to investigate ways of achieving this, and the Early Competition Plan shows great promise. Its main shortfalls are short-term thinking and a lack of joined-up whole-system approach.

Costs of Privatised Electricity in the UK

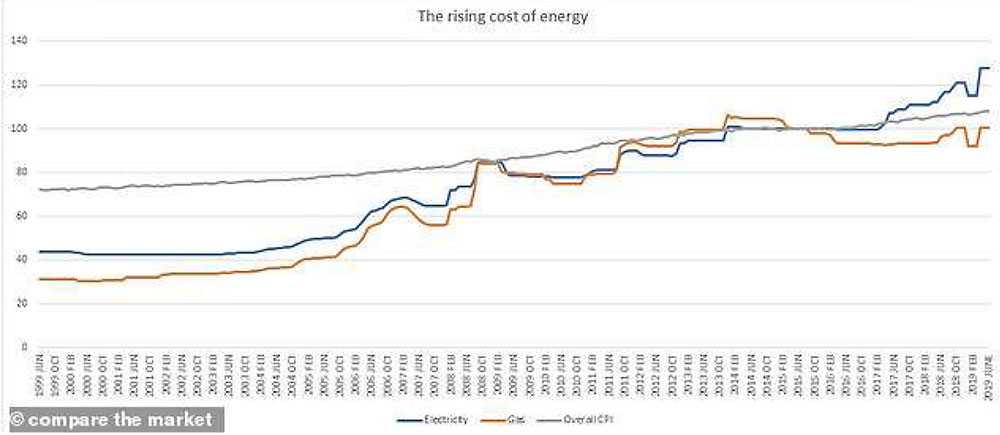

In the years soon after privatising Britain’s electricity system, ministers enjoyed bragging that the country’s electricity was the second cheapest in Europe; now it’s among the most expensive. At privatisation the UK had one of the world’s most reliable and resilient electricity systems; in recent years our grid has been saturated, dependent on imports through interconnectors and subject to black-outs, near misses and ever-escalating costs. This article considers why.

In the years soon after privatising Britain’s electricity system, ministers enjoyed bragging that the country’s electricity was the second cheapest in Europe; now it’s among the most expensive. At privatisation the UK had one of the world’s most reliable and resilient electricity systems; in recent years our grid has been saturated, dependent on imports through interconnectors and subject to black-outs, near misses and ever-escalating costs. This article considers why.

Loss of Focus

The basis for managing and operating the electricity system should be best value-for-money for all consumers, long-, medium- and short-term, with a more-than-adequately reliable and resilient grid. This basis is mostly lost by the mantras developed by BEIS, Ofgem and National Grid, supposedly to deliver it. These mantras include:

- Lowest-cost wholesale electricity, regardless of total system cost, which is why total consumer bills are such a political hot potato now and why Ofgem is involved in setting price caps for consumers.

- Lowest cost now, sacrificing tomorrow’s consumers on the altar of today’s, explained in more detail below.

- Ever shorter-term contracts, preventing large-scale long-term investment without special financial instruments, discussed in more detail below.

- Not “picking winners”, which has been derailed into the mistaken interpretation that no assistance should be given to any developer/technology, instead of offering the same opportunities for assistance to all.

- Competition everywhere (derived from not picking winners) to the point at which developers are greatly discouraged from developing and putting forward imaginative proposals. A level playing-field would be achieved equally by allowing all developers equal access to bilateral negotiations, and agreeing contracts that reflect the modelled capabilities of each plant and adjusted for actual capabilities.

Which Consumers?

BEIS, National Grid and Ofgem continually (including in this consultation) focus on “value for money for consumers” but never define which; in particular, when. Over the last 30 years there has always been a short term focus as opposed to the medium and long terms, sacrificing the consumers of tomorrow on the altar of today.

As an example, the cheapest way to procure energy over a 2-year period is with a 2-year contract. The cheapest way to deliver it is with a fully amortised plant. At the end of the contract, it’s won again in the same way, only the plant is older, more clapped-out, less reliable and more expensive to run. Over a 20-year period, prices rise gradually to be more expensive overall than having let a 20-year contract to start with. And the cheapest way to deliver a 20-year contract is to build a new and better plant, so the longer-duration contract provides for the ongoing renewal and resilience of the electricity system at cheaper overall cost. And the situation is getting worse, with moves towards real-time half-hourly contracts which are, of course, supported by incumbents because they know that it excludes major capital investment and hence new market entrants / competition.

This is why nearly all the major investment since privatisation (other than what was already in the pipeline at that time) has been against special financial instruments such as ROCs, OFTOs, CFDs, CATOs, T-4 Capacity Market etc. But each such instruments has rules and is therefore a market distortion.

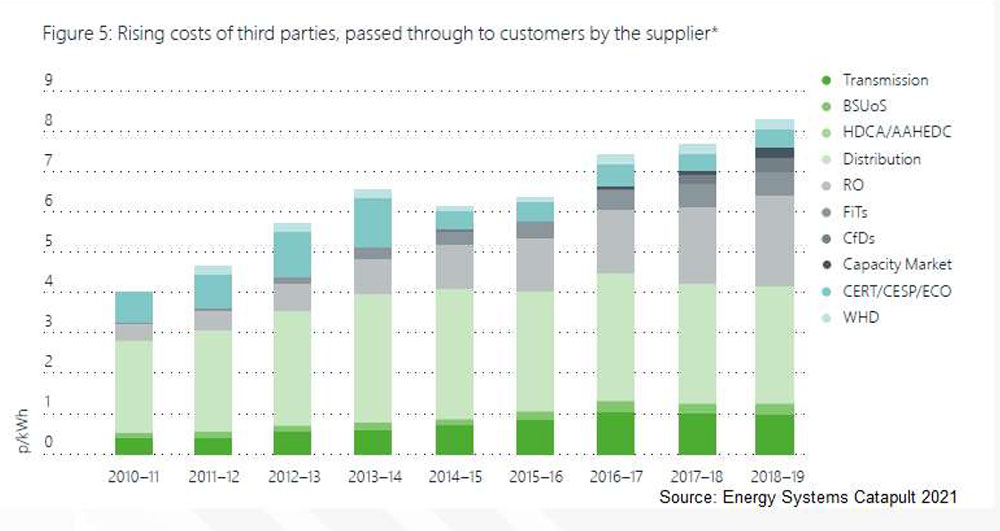

What is Cheaper?

This focus on cheaper electricity costs and short-term asset sweating (known euphemistically as increasing asset utilisation, or investing according to actual rather than forecast need) leads to cheaper wholesale electricity prices. It also leads to letting narrow (salami-sliced) contracts to address individual challenges. However, to ensure that the grid remains adequately supplied, reliable and resilient (and greening), levies and charges have increased inexorably because these matters are not embedded into the market mechanisms. This means that levies and charges are now a greater proportion of the electricity price than are wholesale electricity prices, and this trend/distortion is growing inexorably.

This salami-slicing also favours the narrowly-capable, smaller plants over broadly-capable, larger ones. If a plant can deliver a dozen services, it cannot bank on winning all twelve contracts every time they are built. Therefore it needs to recover its costs on an expectation of the number of contracts it will win (say, eight). This will increase its cost recovery rate by 50%, putting up the prices to consumers; and if the plant wins all 12, it would over-recover by 50% and so earn excess profits which the regulator cannot prevent as it’s the cost of the commercial risk created by the salami sliced system.

This in turn means that the higher-value-added services (such as dynamic containment and frequency/voltage control) are let separately from the harder-to-let contracts (such as longer-duration ones), yet the plants that can deliver the latter need the former in their revenue stacks also; not having the former in their revenue stacks means that they have to recover their costs over only the latter, meaning that the whole-system cost is increased by the value of the former services that the more-flexible plants can also deliver cost-effectively. In other words, the system will be paying for excess higher-value services, and the means for such excess payment will be in the raising of the prices for harder-to-let contracts, so the problem will be mis-identified as high prices for the latter rather than the sourcing of too much of the former from narrowly-capable plants.

Short-Duration Contracts

National Grid has expressed bewilderment that, although market signals have shown over £100m p.a. costs incurred from constraints in the England/Scotland boundary regions, and shown such levels for almost a decade, no plants have been put forward to deal with them. In fact, this should be no surprise: it is due to the short-duration nature of contracts. If a developer were to spend millions on a plant based on the expectation of such revenue streams, there is no guarantee that the next year NG won’t build some assets that remove or reduce them. For major capital investment, the market needs not only market signals but contract durations sufficient to recover costs. And the longer the contract duration, the longer the amortisation period and the lower the contract price – assuming that the asset has sufficient plant life.

Therefore short-duration contracts prevent major capital investment; and disincentivise long-lived plants more than short-lived ones. Hence, for example, the major build-out of 8-year-life batteries when 4-year contracts were offered, and no 40-to-60-year-life inertial storage plant was proposed for such contracts.

Less Reliable

It also means that the country now relies on imports through interconnectors during “times of system stress” (high demand and/or low renewable generation), and will continue to do so for decades to come, according to National Grid’s Future Energy Scenarios and other such analyses from most analysts. This ignores two facts: (a) we can’t rely on imports for our electricity needs, and (b) Brexit. We can’t rely on imports because the energy transition plans of all Western European countries except Iceland, Norway and Switzerland rely by 2040 on imports during such times, which are often concurrent in neighbouring countries: if all are importing, who is exporting. And Brexit means that we can no longer rely on contracts: we have moved from being legally a “domestic” customer to an export market, and it is not conceivable that any grid operator would tell their government that a black-out in a major city was because they could earn a few million euros exporting the energy that that system needed, whatever the contractual constraints. We were forecasting eventual black-outs for these reasons from 2015; the first occurred in 2019 (though primarily due to reliance on synthetic instead of real inertia, and there have been many outages and near-misses both before and since.

Less Resilient

This approach has also led to the loss of resilience, including plants that can regulate the voltage, frequency, reactive power and recovery (including black start) of the grid. True, batteries can provide most of these, but dedicated batteries are needed; a large-scale long-duration inertial storage plant can deliver them concurrently with all the other requirements (balancing, ancillary services, stability services etc.).

And, by National Grid’s own analysis, batteries cannot provide black start. Yet millions are still being spent on chasing this mirage, not only wasting those millions but also distracting the grid and regulatory experts from solutions that will actually work.

Lack of Whole-System Thinking

As the energy transition has progressed, one issue at a time has been identified (lack of new build, inertia, phase-locked loops, black start, voltage/frequency regulation, reactive power/load, wholesale price volatility etc.). These have been addressed one at a time, bringing in narrow contracts that are let separately, with the express aim of bringing new assets into roles supporting the grid. This is great, but such assets are small and of narrow capabilities, delivering only the capability sought and little else. Which in turn makes large and flexible assets impossible to build as their commercial risks are too great, even if they’re exactly what the grid needs and what would deliver best overall value for money for consumers – see the salami-slicing link above.

This siloed thinking misses the fact that the entire suite if challenges has just two causes: short-termism (see above) and the replacement of inertial, dispatchable power stations with asynchronous, intermittent generation. And that the most efficient way to deal with the majority (not all – each technology has its place) of the issues raised is solvable most economically, reliably and resiliently using large, flexible assets, especially large-scale, long-duration, inertial storage which has (to date) not been built owing to all these adverse market and regulatory issues, as well as the regulatory mis-definition of storage. Thankfully, the need for longer-duration inertial storage is starting to be accepted, with the latest Future Energy Scenarios, some other analyses and BEIS’ competition for longer-duration storage; some current consultations are also showing a measure of realisation.

This siloed thinking misses the fact that the entire suite if challenges has just two causes: short-termism (see above) and the replacement of inertial, dispatchable power stations with asynchronous, intermittent generation. And that the most efficient way to deal with the majority (not all – each technology has its place) of the issues raised is solvable most economically, reliably and resiliently using large, flexible assets, especially large-scale, long-duration, inertial storage which has (to date) not been built owing to all these adverse market and regulatory issues, as well as the regulatory mis-definition of storage. Thankfully, the need for longer-duration inertial storage is starting to be accepted, with the latest Future Energy Scenarios, some other analyses and BEIS’ competition for longer-duration storage; some current consultations are also showing a measure of realisation.

Replacing this siloed, short-termist, blinkered thinking with long-term, whole-system thinking, evaluation and contracts will deliver a system that will address today’s needs, develop proactively for tomorrow’s, and be cheaper for consumers in the medium and long terms; potentially also for short-term consumers.

Short-Term Thinking

The entire process of planning and regulating the grid is exceedingly short-term. The longest vision, NG’s Network Options Assessment, focuses on a 10-year timescale; with such thinking, the grid would never have been built in the first place, leaving the entire economy struggling and held back. An example of such short-termism was the much-touted (though, thankfully, not achieved) “second dash for gas” to achieve 2025 emissions targets even though 2030 emissions targets would have turned most such power stations into stranded assets. The only way to avoid such waste is to prioritise 30- and 50-year timeframes – which will ensure a cheaper, more reliable and more resilient grid in those timescales without increasing greatly the cost to today’s system/consumer.

As most grid-connected assets that are developed today will still be operational in 2050, all new developments must be one of:

- 2050 compliant (i.e. emissions-free);

- Convertible to 2050 compliant; or

- Short-life assets that will be replaced before emissions targets exclude them from markets.

If short-life assets, emissions relating to disposal and replacement should be taken into account, as should global resource availability in comparison with forecast global demand, e.g. lithium, cobalt and rare-earth metals.

Proactive Grid Development

It is worth recalling that the grid was only built because of whole-system, long-term thinking. For that reason, it was developed and extended based on forecast rather than current needs. This has been caricatured politically as “gold-plating the grid”, with a focus over the last decades on increasing utilisation. But in reality,

- Building the grid in a measured and rational programme ahead of need is as much as two-thirds cheaper than building it reactively against need, as discovered in Australia; the Electricity Networks Association can cite excellent examples from South Australia and elsewhere, to support this statement.

- Even if such demand did not materialise at the expected time, it has materialised since, so the benefits of investing in such more rational and measured ways greatly outweigh the small number of years for which a given part of the grid was under-utilised.

- And the current method means that now there are large and unknowable numbers of projects that are just not being proposed because of the cost of reinforcing the grid to accommodate them, slowing down the energy transition and reducing the quality of the entire system.

Excessive Costs for Consumers

The result of all this is that system costs are rising so fast that a pro-market government has instructed a market regulator to intervene in the free operation of markets by imposing a cap on consumer electricity prices.

The poor design of market mechanisms means that all manner of levies and charges are added to electricity bills. A couple of decades ago, these totalled under 25% of consumers’ bills, paying for grid upkeep, and balancing and ancillary services. Now they account for over 50% and still rising inexorably. This in turn means that plants are deriving a majority of their revenues from activities other than providing energy and the services necessary to maintain the grid, distorting market price signals; the price cap distorts them further.

The poor design of market mechanisms means that all manner of levies and charges are added to electricity bills. A couple of decades ago, these totalled under 25% of consumers’ bills, paying for grid upkeep, and balancing and ancillary services. Now they account for over 50% and still rising inexorably. This in turn means that plants are deriving a majority of their revenues from activities other than providing energy and the services necessary to maintain the grid, distorting market price signals; the price cap distorts them further.

Intermittency and asynchronicity are both major disturbances for the grid. Unless large-scale renewables are matched (and, preferably, connected to the grid through) similarly large-scale, long-duration, synchronous (i.e. naturally inertial) storage, then when renewables penetration exceeds about 16%, the non-energy costs of managing the grid start to go up exponentially: below that figure there is enough power station output to balance and compensate for the intermittent, asynchronous renewables. Above that figure there is both declining power station capacity and growing renewable generation, so the disturbances grow while the ability to compensate for them shrinks.

An Alternative Approach

There is a very simple alternative approach to the regulation and contracting a 21st-century electricity system, which can be implemented step-by-step rather than as a “big bang”. Not only will it deliver the major capital investment required by the system, and the total systems cost reductions, but also new technologies, innovation and “cleanness” (lack of emissions and other pollutants, and could include other considerations such as resource scarcity) can be incentivised without a penny of subsidy.

If the government then wishes to encourage the development of other technologies, any funding would be entirely separate and additional. This would reduce greatly the cost of such public funding, as it would only have to cover a proportion (subject to match funding) of the difference between commercial and developmental costs.

Matched with this are other ways to incentivise R&D, first-of-a-kind plants and clean technologies, by the finance ministry and others. The more such measures are combined, the more affordable, reliable and resilient will be the energy transition and subsequent Net Zero energy system.