Index

Contents

Introduction 1

Batteries and DSR on 9th August 2

Interconnectors’ Response 3

The Future of Interconnectors 3

Need for Back-up 5

Brexit 6

Providing Resilience – Types 7

Providing Resilience – Quantities 8

Grid Stability Services 9

Disincentivisation of Storage 10

Grid Capacity 11

Conclusions 12

Actions 12

Footnote: Enhancing European Industry and Exports 13

Appendix 1: Energy Supply and Demand 14

Appendix 2: Carbon Capture, Use and Storage 17

Appendix 3: Salt Basins and Other Geologies for CAES 18

Appendix 4 HM Treasury Discincentivisation of Storage 21

Appendix 5 Regulatory Definition of Storage 25

Appendix 6: Scale of the Problem – TINA 30

For questions, contact Mark Howitt, +44 7910 020 686, mhowitt@storelectric.com

Introduction

As is well known, on Friday 9th August the electricity supplies from one wind farm (Hornsea One, 750MW) and one gas-fired power station (Little Barford, Cambridgeshire, 680MW) failed almost simultaneously at 16:54. The total capacity loss was ~1,430MW at the beginning of the evening peak. While National Grid’s power was restored by 18:00, disruption continued throughout the evening on the transport networks.

These black-outs have long been predicted by some in the electricity industry as being direct consequences of the inadequate investment in storage – and especially large-scale long-duration storage – to provide cost-effective and adequate back-up to intermittent (and non-inertial) renewable generation. The same voices predict that such black-outs will become increasingly frequent and severe. And while focusing naturally on the UK, this analysis has broad lessons for other EU countries.

This report also looks at some of the main reasons why the grid has not adapted to its de-carbonisation in ways that would prevent such occurrences in future, from which policy and regulatory conclusions can be drawn.

Batteries and DSR on 9th August

I have read and heard a number of presentations and analyses by battery promoters projecting that batteries were the heroes of the day, providing hundreds of megawatts within 5ms – 2 seconds, if only they hadn’t been overwhelmed by subsequent trips. But that 5ms – 2 seconds delay is what caused the subsequent trips, which shows that batteries contributed to the problem more than they did to the solution on that day. The solution would have been inertia – and Storelectric’s CAES is inertial storage that also offers Synchronous Condenser capabilities 24/7 at the rated power.

In greater detail, despite the proclaimed benefits of batteries and Demand Side Response (DSR), they failed to provide the required resilience on 9th August. This is for a number of reasons, probably including:

- Inadequate scale: typical battery and DSR installations are (even when aggregated) of the order of 1-20MW while the system need was 1.43GW;

- Inadequate duration: the outage was longer than the duration of most battery and DSR services;

- Battery state of charge: National Grid’s plans appear to assume that batteries are always kept fully charged, whereas in reality they are all cycling in charge-state according to their contracts and commercial optimisation;

- Battery and DSR activation times: even if perfectly available, the fact that batteries and DSR (and gas reciprocating engine plants) need to be activated actively imposes delays in response of a few seconds, during which delays the system fails, whereas inertial systems are an always-on response;

- DSR response times: DSR resources need to be polled, signal availability, and then receive and respond to an activation signal, which increases their response times still further.

Lesson for other EU countries: many EU countries are relying on DSR as part of their response; this reliance needs to be re-considered in this light. There is a real and excellent role of DSR, namely to minimise the cost of supporting short-duration spikes (upwards or downwards) in supply and/or demand, but it is suitable neither for longer-duration support nor instantaneous response.

Second lesson for other EU countries: What is really needed on the system for short-term response is real inertia, such as can be supplied by large-scale long-duration storage especially if it also operates in synchronous condenser mode.

Interconnectors’ Response

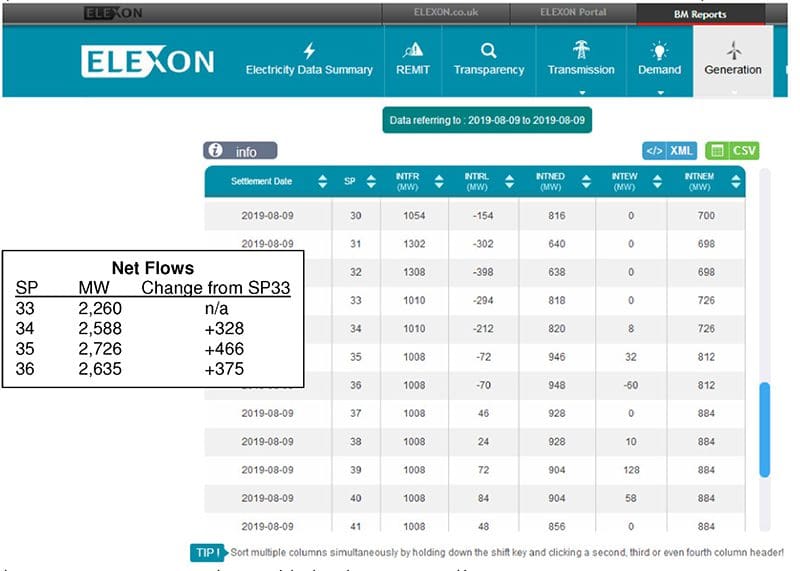

The industry has been declaring for many years that interconnectors would provide back-up to renewable generation. However the actual interconnector response was a fraction of the 1.43GW needed:

(16:54 is in Settlement Period 33; 18:00 is the end of Settlement Period 36.)

Interconnectors can only provide back-up power if:

- They have suitable contracts or arrangements with foreign generations, AND

- They have sufficient un-contracted capacity to carry the additional energy.

This therefore constitutes proof that interconnectors cannot be relied upon even under existing trading relationships and ignoring future Brexit-related disruptions to those relationships.

The Future of Interconnectors

The above sections focus on the immediate responses both required and (not) provided. This section considers the other end of the scale of response: longer duration sustained back-up power.

All National Grid’s Future Energy Scenarios 2019 (FES 2019) rely on increasing amounts of interconnection to provide for actual demand and supply margin (see next section).

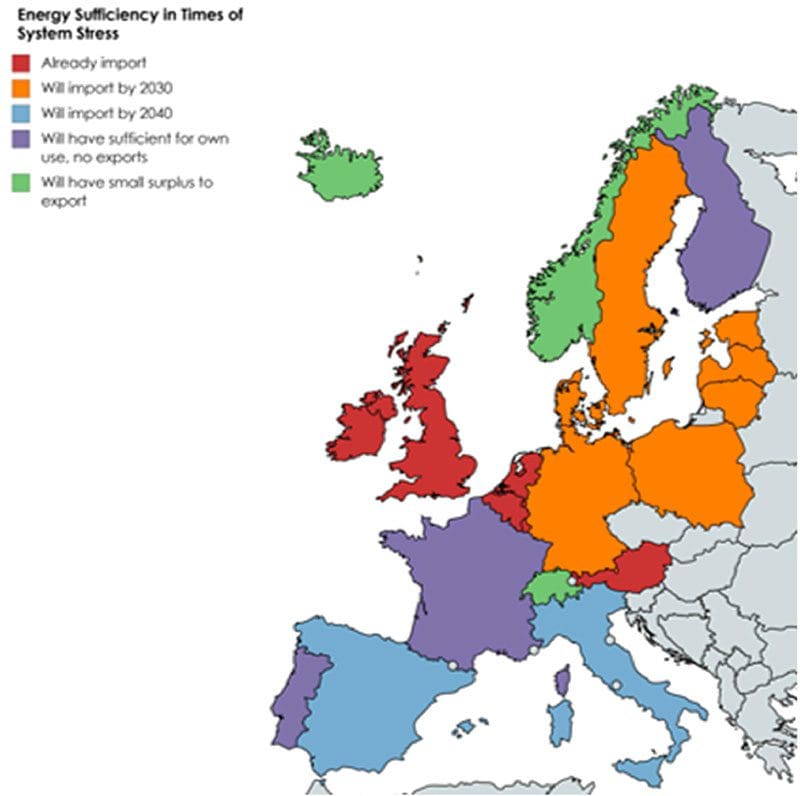

We have studied the energy transition plans of 6 countries in detail (UK, DE, FR, IT, ES, NL – who account for 75% of EU GDP – please forgive the number of abbreviations!) and are aware in general terms of the plans of most of our other neighbouring countries. As can be seen from the map, during “times of system stress” (i.e. high demand and/or low renewable generation) the UK, NL, BE, EI and AT already rely on electricity imports through interconnectors. By 2030 these will be joined by DE, PL, SE and the Baltic states. By 2040 Spain and Italy will join them. France and Finland will have enough for their own needs due to nuclear, and Portugal due to hydro – but no surplus to export. Only Norway, Switzerland and Iceland will have electricity to export – and a 1GW interconnector to Iceland is expected to cost more than £5bn.

Given that these “times of system stress” are largely concurrent (e.g. after sunset on a windless winter evening), this means that there will not be enough spare electricity for all the countries that rely on the imports, yielding rolling black-outs and brown-outs (euphemism: enforced DSR) in all of them. And in terms of prioritising who gets the trickle of exportable electricity, a no-deal Brexit means that for the first time ever, our neighbours can tell us “I don’t care how much you’re offering to pay – our consumers are more important to us than are yours”.

So the only way for each of these importing countries to keep the lights on, and especially for the UK to do so, is large amounts of large-scale long-duration storage.

Lesson for other EU countries: The same issue that today is challenging the UK will also challenge all other countries that do not plan to have at least enough baseload + dispatchable energy for their own needs. If the country were to enter into contracts that ring-fence suitable large-scale long-duration storage resources in another country for its use (e.g. Germany contracting with Norwegian pumped hydro) and that ring-fence interconnector capacity to import it, then such capacity can be included in the calculation; if either of these elements (contracted storage, and interconnector surplus capacity) are missing, then it cannot.

Second lesson for other EU countries: Similarly, interconnectors are only useful for back-up inasmuch as there is (a) sufficient spare energy at the other end at the appropriate time, and (b) sufficient spare un-contracted capacity to carry it. The latter must be paid for, otherwise commercial considerations will maximise their utilisation and minimise unused capacity, thereby jeopardising back-up capability.

Need for Back-up

FES 2019 makes evident that this is the first year in which the United Kingdom does not have sufficient domestic baseload and dispatchable generation for its actual peak demand, without even considering the supply margin which exists to cope with energy shocks like the outages of 9/8/19. Most countries calculate that a suitable supply margin is 15% of peak demand, i.e. ~9GW using peak demand of 60GW; though 10% is considered manageable without excessive numbers of outages.

Looking to the future, under every scenario, interconnectors are used for both peak demand and supply margin for the indefinite future – and under all scenarios, forecast interconnector capacities are inadequate even for that. See Appendix 1 for further details.

Given the outages of 9th August, this means that current plans are guaranteeing black-outs in large parts of the country. And looking at the future energy scenarios, these guaranteed black-outs are planned to become increasingly frequent and severe.

Lesson for other EU countries: Most other EU countries’ energy transition plans rely equally on imports of electricity during times of system stress, as described above. This needs to be analysed and addressed for each country; we have analysed those of UK, DE, ES, FR (previous PPE only), IT and NL.

Brexit

Currently Britain is in the single market, regulated by the European Court of Justice. This ensures that if we pay enough, our neighbours have to sell us the electricity, and to do so tariff free. According to FES 2017, “our analysis currently assumes tariff free access to EU markets under all scenarios.” This is the rosiest possible scenario, which is therefore a very rash assumption – and the more so as the government has consistently said that we will leave both the single market and the jurisdiction of the European Court of Justice. Worse, this means that all our neighbours would then be free to tell us that they prioritise their consumers at any price.

Lesson for other EU countries: Most EU countries have similar issues of unavailability of energy to import, though they do not have the contract-enforcement issue of a no-deal Brexit.

Providing Resilience – Types

Given that the UK cannot rely on interconnectors, we need to provide resilience domestically.

Supply can be divided into the following categories:

- Baseload: always-on, e.g. coal, nuclear, some hydro;

- Dispatchable: variable according to demand, e.g. gas power stations and peaker plants, biomass, remaining hydro;

- Large-scale long-duration storage, e.g. pumped hydro, Compressed Air Energy Storage (CAES);

- Smaller-scale short-duration flexibility, e.g. grid-connected batteries, Demand Side Response (DSR);

- Interconnectors.

Interconnectors cannot provide reliable back-up services, as we have seen. Their proper role is therefore to moderate prices and price fluctuations in the normal operation of the grid.

Given that times of system stress usually last for many hours, and that typical durations of batteries (20-16 minutes) and DSR (15-30 minutes) are much briefer, they cannot provide such back-up services either. Their small scale implies the same. Their proper role is to provide cost-effective short-term flexibility response.

Large-scale long-duration storage needs to be at least 4 hours’ duration (as recognised by Capacity Market de-rating rules) in order to provide such back-up services. Therefore these, together with baseload and dispatchable generation, can provide the resilience the country needs.

Future volumes of baseload and dispatchable electricity currently rely on widespread roll-out of Carbon Capture, Usage and Storage (CCUS) technology. We would discount these assumptions for a number of reasons, including:

- Too expensive per installation – even America can’t afford to build one;

- Too expensive nation-wide – CO2 pipelines would have to be constructed across the country, at ~£1m/km plus lead times for planning and construction;

- Too inefficient generation – imposes a ~30% efficiency penalty on the power station;

- Too inefficient capture – all projects consider only 80% capture of the emissions to even stand a chance of future commercial viability, which leaves the other 20% uncaptured, for which grand assumptions must be made about widespread implementation of the even-less-certain and less-commercial BECCS (bio-energy CCS) despite the fact that the world has insufficient farmland to sacrifice to biomass generation at such a scale;

- Uninsurable – not even the European Union will insure against the risks of leakage from CO2 stores, which endure for millions of years until the tectonic plates are subducted;

- Usage is only postponement of emissions, not sequestration of them, so only CCS can be counted;

- Too uncertain – current plans aspire to develop commercially viable technologies within a decade, with the build programme then subject to the normal delays (finance, planning and other permitting, design, construction not only in power stations but also of CCS infrastructure including pipelines across the country); our need is much more urgent than that.

Lesson for other EU countries: The above analysis applies equally to other EU countries. For more information, see Appendix 2.

Providing Resilience – Quantities

The power rating (MW) of resilience that the country requires is simple to calculate:

baseload + dispatchable + long-duration storage ≥ demand + supply margin

Therefore the power rating (MW) of large-scale long-duration storage required is

long-duration storage ≥ demand + supply margin – baseload – dispatchable

The energy capacity (MWh) of such storage is also easy to calculate, though there are two methods. Essentially the resilience needs to accommodate the longest period for which generation is likely to be negligible, which the French and German energy transition plans have identified as a 2-week weather pattern called (in German) the kalte dunkel Flaute (cold dark doldrums) which over-lie most of the continent for up to a fortnight mid-winter (i.e. during the annual peak demand period), about every couple of years; if the durations are reduced to days, and geography to a few countries, then these patterns are frequent. All the terms in the two equations below refer to the total energy over the fortnight.

The simple one applies where demand never dips below the sum of baseload and dispatchable:

long-duration storage ≥ demand – baseload – dispatchable

The more complex one allows for baseload and dispatchable generation to top up storage capacity, though this stored energy can only be accounted for at the round-trip efficiency rating of storage:

long-duration storage ≥ demand – baseload – dispatchable – stored generation

where stored generation is:

Total generation (baseload + dispatchable) that exceeds demand at any time during the period in question, multiplied by round-trip efficiency of storage

Note that the UK exports to Ireland during peak demand times. If this is to continue, such exports need to be added to domestic demand in all the calculations above.

The location of the storage is also important. Pumped hydro (both current and potential) is mostly in remote parts of Scotland and Wales, remote from both supply and demand. Given that the outages of 9th August occurred in the east of England, these would hardly have helped – especially given the lack of excess capacity on the grid (see Grid Capacity, below).

CAES can currently be implemented in most of the country’s salt basins – see Appendix 3 for British and EU salt basins. These are well distributed, and well located for both supply (areas designated for wind farms are shown on the map) and demand (selected cities are shown). There is also consideration of other geologies in Appendix 3. Therefore CAES provides the best potential for back-up.

A final consideration is cost: depending on location, CAES costs less than one-third of the cost of a new pumped hydro installation, without the need for such extensive extensions to the grid. And while doubling the size or duration of batteries increase their capital costs by roughly 75-85%, doubling the size of CAES increases cost by 50% and duration increases it by 30%.

Lesson for other EU countries: The above analysis applies equally to other EU countries, for which salt basins are also mapped in Appendix 3.

Grid Stability Services

National Grid have recognised enormous issues with the loss of inertial generation. Inertia enables the system to ride through any sudden changes in voltage, frequency etc., giving time for other assets to respond and so avoiding disruption. They are trying to address many of them through their Stability Pathfinder project. This is a huge advance on previous attempts to address the issues one at a time through individual contracts for each of the dozens of consequences of loss of inertia, e.g.:

- Enhanced frequency response;

- Reactive power;

- Increasing use of balancing and ancillary services (see projections from Aurora below).

The inadequacy of this response and inevitability of consequent black-outs has been predicted consistently for a number of years by some parties.

How much better to address the cause of the problem, which the Pathfinder may succeed in doing, by providing contracts that enable inertial systems (especially inertial storage, like pumped hydro and CAES) to be built.

Lesson for other EU countries: Every single country has the same issues of loss of inertia due to de-carbonisation. Some may have sufficient hydro / pumped hydro (e.g. Norway, Switzerland) and/or nuclear (e.g. Finland, France) to accommodate such decarbonisation without substantial measures to address inertia and consequential services, but all the rest need to address it directly.

Disincentivisation of Storage

Therefore large amounts of large-scale long-duration storage is needed to:

- Prevent black-outs such as occurred on 9th August;

- Provide on-going resilience to the grid;

- Balance increasing amounts of renewable generation;

- Provide grid stabilisation services;

- Reduce the cost, difficulty and lead time of de-carbonisation.

Despite this enormous need for storage, it is disincentivised in many ways, many of which are detailed in Appendix 4 HM Treasury Disincentivisation of Storage, and Appendix 5 Regulatory Definition of Storage.

In a positive recent development, National Grid’s FES 2019 recognises the need for large amounts of large-scale long-duration storage, but still not to the extent of the government’s own 2015 Technology Innovation Needs Analysis (TINA) which identified that, to balance variable (as opposed to baseload) demand alone the country needed 27.4GW of new storage with an average duration of 5 hours, by 2030. See Appendix 6 for further information.

Lesson for other EU countries: Different countries have different disincentives for storage, but major such disincentives exist in all the countries we have yet analysed. The wrongful regulatory definition of storage is Europe-wide, together with its malign consequences. Lack of recognition and remuneration of inertia is continent-wide. Cap-and-floor regimes greatly reduce arbitrage revenues and signals, distorting markets and reducing storage profitability. Each country needs to look at its own regimes and level its own regulatory / contractual playing-field.

Grid Capacity

Ever since privatisation, governments have tasked Ofgem with maximising grid utilisation and minimising construction of grid assets ahead of need in the name of avoiding “gold-plating” the grid and thereby minimising its costs to consumers. However the asset-sweating strategy regarding the electricity grid is greatly impeding investment and decarbonisation.

- If 10,000 EVs were projected for each of Warwick and Leamington Spa, and in fact 15,000 were to be bought in Warwick and 5,000 in Leamington, the grid would be totally disrupted and unable to cope: our forecasts are too inaccurate (numbers of EVs in 2018 are over 40 times the forecast 10 years before, if I remember correctly), so we must build excess capacity because of the lead time to construct grid reinforcements.

- As the ENA (Electricity Networks Association) will tell you, there is a case study in Southern Australia where investment was deferred as being too expensive; when the need became critical just a couple of years later, it cost three times as much to undertake the work as an emergency programme – so even if a small proportion of the built-ahead-of-need assets prove unneeded, the overall programme cost is greatly decreased by building ahead of need.

- The time and cost to build and install new grid connections is so great that many useful and excellent projects are not proposed: it is not only the direct costs, but the indirect costs of tying up money and resources for extended periods.

- There is a regulatory and governmental obsession that National Grid “gold-plated” the system, but in fact almost every asset built then has proved useful even if that use has come a few years later than the original forecast.

- If we had only built to proven need, the National Grid would never have been built.

- The short-sighted focus on meeting 2030 targets is failing to put in the investment and incentives required to develop, test and roll out the technologies required to meet our 2040 and 2050 targets.

The outages of 9th August may provide another perspective: did grid constraints reduce the ability of other plants to provide electricity in the required quantities, to the required locations? Since grid capacity is targeted at 97% utilisation during peak times, and many parts of the grid are loaded above this, a lack of headroom is suggested. Did it have the capacity to deliver 0.7-0.8GW electricity to each of these locations, from where such surplus generation (or importation) was available?

Instead, the government and all regulators and departments should determine their 2050 objectives, together with alternatives, and undertake / incentivise all investments into plant, networks and technologies accordingly. They should structure all contracts and regulations to deliver this. Otherwise the costs of the energy transition will become unacceptably high to the entire country, and be passed onto either government as subsidies or consumers as charges – or both.

Conclusions

The conclusions to which we are driven by the events of 9th August, and by their analysis in the context of future plans for the energy system, do not just affect the UK but also most other EU countries. They include:

- Interconnectors cannot provide the resilience needed by the grid;

- Nor can batteries and DSR;

- It would be both unsafe and premature to rely on CCUS generation;

- An extensive roll-out of large-scale long-duration storage is needed, which would also provide the inertial power that in turn provides the requisite grid stabilisation services;

- CAES can provide large-scale long-duration storage much closer to both supply and demand, in a better-distributed manner, and much more cheaply than pumped hydro;

- There are numerous disincentives for large-scale long-duration storage which need rectifying, most notably the regulatory definition of storage which should be as storage (based on the definition of interconnectors) rather than as generation;

- The grid also needs to be extended ahead of need, to minimise cost and disruption.

Actions

- Plan to enable the any grid to operate independently of any other country (potentially including some interconnector demand from neighbouring countries that will continue to be supported, e.g. Ireland supported by the UK), providing its own generation and balancing services;

- Define storage as storage, in primary legislation;

- Incentivise the construction of many large-scale long-duration storage projects, sufficient to balance the grid domestically;

- Contract with such storage to provide storage services, rather than an ever-increasing stack of salami-sliced services;

- Pay for inertia itself, in preference to the many consequences of not having it;

- Change policy to build grid capacity ahead of need, based on plans and forecasts, to reduce construction costs and enable development of energy-transition assets.

Footnote: Enhancing European Industry and Exports

As a footnote, doing this could create a European large-scale long-duration storage industry that would enhance the country’s economy and exports, leading the world: it already has a number of companies that are in such leadership positions if only the regulatory and contractual playing-field were levelled and they were able to build first-of-a-kind commercial plants.

Appendix 1: Energy Supply and Demand

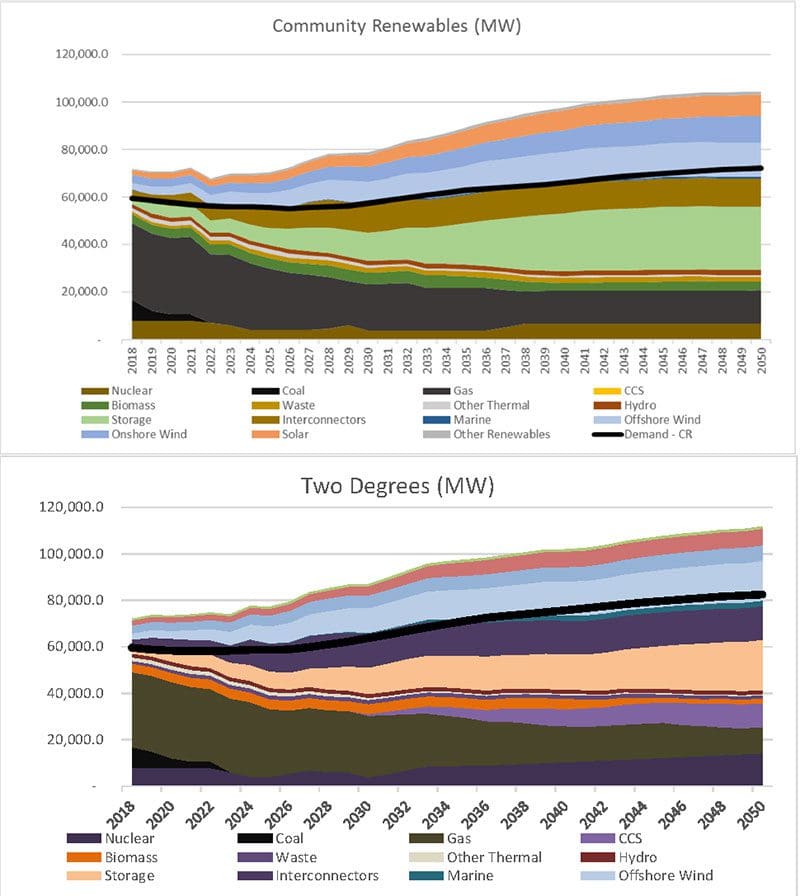

Energy supply and demand in the Community Renewables and Two Degrees scenarios of National Grid’s Future Energy Scenarios 2019. These are the only two scenarios compliant with the Climate Change Act, and since the enactment of the Net Zero targets, have become conservative scenarios.

The above graphs are all FES 2019 figures, with the bars re-sequenced to show baseload at the bottom, then dispatchable, then interconnectors, and finally (in decreasing sequence of reliability) intermittent generation. These are listed by de-rated nominal capacity: as discussed elsewhere, duration of storage is not reflected in these figures. Storage should be represented by 2 bars, short-duration (<2 hours) and long duration, in order to get a good understanding of the energy system.

These graphs can be summarised as:

This looks like a serious risk: the country is depending on imports for actual demand, without even taking into account either supply margin (10-15% to be added to demand) or the lack of duration of most of the storage concerned.

However, when de-rating factors are applied to the generation mix, it looks absolutely impossible:

Actual demand, excluding both the above factors, exceeds the country’s capacity both to generate and to import. Even assuming that imports are available, which is highly unlikely during times of system stress.

Appendix 2: Carbon Capture, Use and Storage

CCS remains unaffordably expensive, much more so than nuclear: £27bn p.a. plus capital costs for 8MW abated coal fired power stations, without allowing for the inefficiencies introduced into the power generation process, according to aspirational figures from DECC’s website which they removed when cancelling the two CCS power station projects in 2015. The introduced inefficiencies increase coal burn by around a quarter, raising its levelised cost of energy to well above that of other generation technologies.

Moreover, the In June 2017 the Americans cancelled the Kemper coal gasification and CCS project when its capital cost for a 582MW plant exceeded $7.5bn, i.e. $12.9bn/GW. If the Americans can’t get it up and running despite paying considerably more than Hinkley Point (which is £20bn for 3.2GW, i.e. £6.25bn/GW or $8.4bn/GW), then what hope do we have of doing so?

Usage is at a very early stage of development, with some promising lines of development – however these are all at very early (mostly theoretical and laboratory) stages. And most of them result in the re-emission of the CO2 later on. The UK parliament has released a briefing on this. Therefore usage does not carry promise of major CO2 emissions reduction in the near future, so the principal target for national emissions reduction must remain CCS.

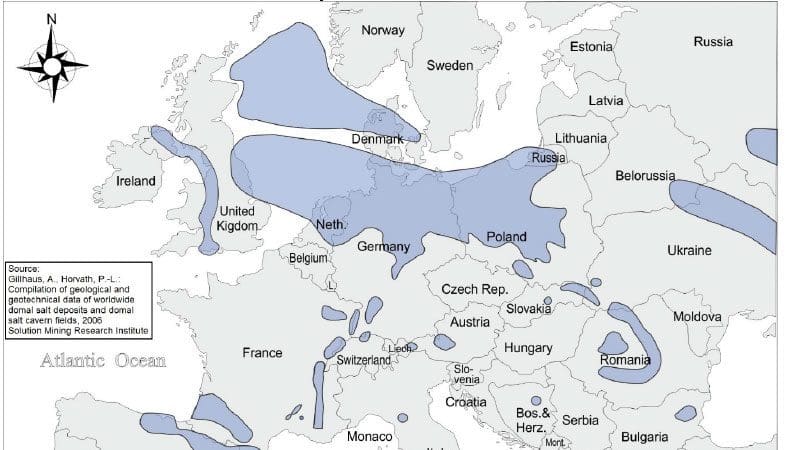

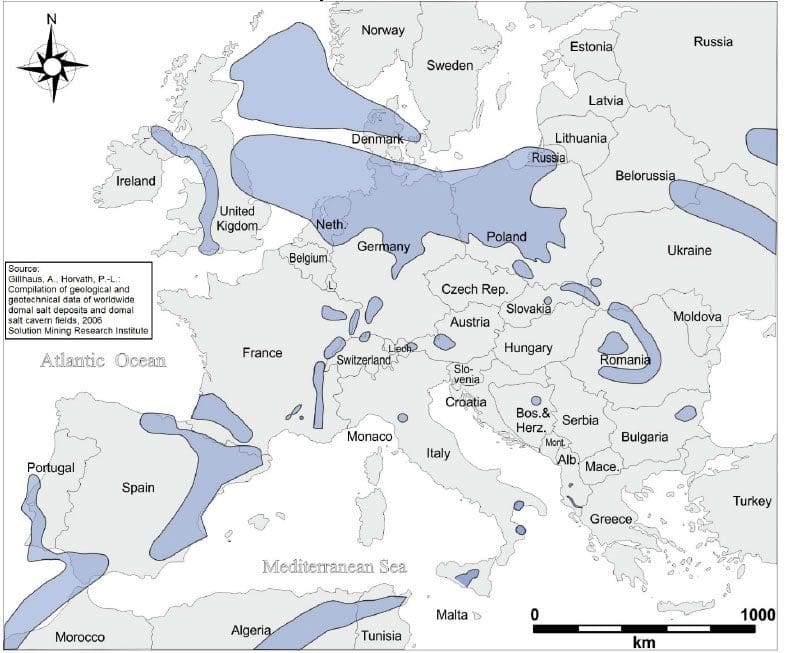

Appendix 3: Salt Basins and Other Geologies for CAES

Locations of Salt Basins and Wind Farm Designated Areas in the UK

Salt basins are shown in yellow and pink. Areas designated for wind farms are shown as blue ovals.

The Lancashire salt basin (circled, near Fleetwood above Liverpool and WNW of Blackburn) has capacity for ~20GWh onshore.

Stafford and Worcester basins may not be sufficiently deep or thick.

Offshore salt basins are not shown, and are much more extensive.

Locations of Salt Basins in Europe and North Africa

There are salt basins in most EU countries; particularly well-endowed countries are Denmark, France, Germany, Poland, Portugal, Romania and Spain; Austria, Italy and Slovakia also have substantial deposits.

Other Geologies

Salt basins are only one of the geologies that are potentially usable for CAES: others include aquifers (both sweet and saline, too deep for drinking water) and depleted hydrocarbon wells (both oil and gas), collectively known as “porous rock” geologies. These other geologies each have a series of challenges before they are usable, and Storelectric has ideas as to how to overcome those challenges, but it needs work, time and investment. Salt caverns are the easy, well-known geology for CAES.

Porous rock geologies, when developed, will be more suitable for longer-duration storage. But they will never displace salt cavern storage as they address different parts of the market: caverns are better for fast-in fast-out, 4-12 hours’ duration; porous rocks for baseload and longer durations.

Appendix 4 HM Treasury Discincentivisation of Storage

Input to HM Treasury Select Committee Review June 2016

Her Majesty’s Treasury has many ways in which it is impeding decarbonisation. This document focuses on the electricity system, because that is the scope of Storelectric’s work. Storelectric is seeking to build innovative large-scale long-duration storage on the UK electricity system, and to build up a UK-based industry to address a multi-trillion dollar market with world-leading technology, but has been stalled for 6 years in doing so largely by Treasury disincentives. These split into two main categories: finance, and energy.

Energy

The government defines storage as consumption plus generation, meaning that all charges relating to both are applied to it, thereby triple charging storage for (for example) grid access and climate levies. Generally people talk about double charging (for import and for export of electricity), but the electricity purchased by storage already has those charges applied; therefore it is triple charging.

Energy storage generates no new electricity. It just moves electricity in time very similarly to interconnectors moving it in space: from when it’s not wanted to when it is, while interconnectors move it from where it’s not wanted to where it is. Therefore storage should be defined as storage, a grid service, based on the definition of interconnectors.

Treasury effects of this include that storage does not qualify for EIS or other investment incentives, thereby penalising it by redirecting funds that would otherwise be willing to invest. They are largely redirected into industries that don’t help decarbonisation or the future of the country, whereas storage does.

The regulatory and contractual system for electricity is also exceedingly short-sighted, and has already resulted in higher electricity costs than neighbouring countries, together with the grid’s assets aging greatly, and the need for any new strategic investment to be incentivised by a market-distorting special financial instrument. It would be relatively simple to construct a system that incentivises major capital investment, clean energy and the introduction of new technologies without costing a penny more in overall system costs. Please see the associated document “A 21st Century Electricity System”.

Finance

Treasury’s incentives for entrepreneurship and investment are all regardless of technology risk. Therefore, following good principles of financial management, because benefits are unrelated to whether or not financiers and investors take on technology risk, they don’t. This means that private sector funding (especially at larger scales) is not available for innovative industries, businesses and technologies. This means that we can finance a chain of restaurants or shops, but not innovative industry that can help UK PLC to grow.

Human beings define technology risk as any risk that is of a technical nature. But financiers define it as anything that hasn’t been done before. This means that if I were to propose a cotton shirt with a plastic collar, they would define it as technical risk. But humans know that there’s no technical risk involved (tens of thousands of sweatshops can make them), but that it’s a commercial risk as nobody would buy them. Financiers’ definitions need changing, because their entire philosophy and strategy are based on it and on risk aversion.

This risk aversion itself needs to be addressed by Treasury incentives. This is not an argument for additional money, but a change in the award definitions to incentive investment in prototypes and first-of-a-kind commercial products/plants. It would be worth considering allowing some mitigation of a first-of-a-kind plant’s costs as a tax break, given that follow-on plants will almost always be more reliable and efficient. It applies to EIS investments, tax breaks for financial funds including pension schemes, R&D tax credits, etc.

A consequence of this aversion to technical risk, and the lack of incentivisation to take it on, is the de-stabilisation of the entire financial system. There are trillions of funds in any currency seeking “safe” investments. Nothing is considered safer than property – except a diversified portfolio of it, so everyone rushed into a sub-prime mortgage investment bubble. When that burst, they all sought the next safest investment and piled into SE Asia, creating another bubble that burst 2-3 years later. It keeps looking for safe investment after safe investment, de-stabilising each by the massive in-flow of too much money seeking too few assets in the category. If some of this money were redirected into innovative industries, not only would those industries be funded and lead national and world growth, but also the other industries would be re-stabilised by the re-balancing of risk and reward.

It would greatly help if funds were given a credit on condition that at least 5% of the fund is invested with significant and auditable technical risk. This means that 95% is still invested “safely”, while 5% (which is a big sum when applied to trillions) goes into new technologies and their commercialisation, with the possibility of much higher returns. By all means, ensure that this money (to qualify) is invested in the UK.

We have had innumerable expressions of interest to finance follow-on plants, but not one to finance our first. For decades, British industry as a whole has been great at invention, but terrible at commercialisation – exactly for this reason. A decade and a half ago the US Secretary of State for Defense stated that one-third of all their new technologies are invented in Britain. They have to go to America to be commercialised, because there is no significant money available for doing so in Britain, for this reason. Given the trillions of pounds washing around our financial systems, this begs the question as to how (when the country was much poorer) we financed the Industrial Revolution.

Government’s Clean Growth Strategy

The government’s Clean Growth Strategy is very short-sighted and is leading the country into huge additional costs for that reason. For example,

- Investment in many interim solutions such as fracking and encouragement of a second dash-for-gas is helpful in achieving our 2030 goals of reducing emissions, but every one of these new assets would be stranded by 2040 or 2050 because the need then is to eliminate emissions.

- This is leading to a pious faith in magical solutions such as biomass energy with carbon capture use and storage (CCUS). There is insufficient land on the planet for that amount of biomass. And CCUS is so expensive (without considering the 30% “hit” on power station efficiency) that even in America every single project has been killed before construction: if they can’t afford it, what hope have we? Finally, nobody has solved the insurance question: CO2 is heavier than air, so if any North Sea storage were breached (e.g. by earthquake), the resultant burp of CO2 would hover on the water asphyxiating anyone in ships above. This risk remains until the tectonic plate is subducted. All 6 North Sea countries decided that this was too great a risk for any country to bear, so asked the EU to do so. The EU looked into it carefully and said that they couldn’t. The Peterhead and White Rose CCS projects were cancelled a fortnight later: coincidence?

- Incrementalism in (for example) adding hydrogen to gas grids will result in multiple conversion programmes like the transition from town gas to natural gas in the 1970s as the combustion characteristics of the gas will be different as the hydrogen percentage increases; what’s needed is a leap to 100% hydrogen in one part of the country (with a single conversion project), gradually to be rolled out elsewhere. That is merely one example.

- The asset-sweating strategy regarding the electricity grid is greatly impeding investment and decarbonisation.

- If 10,000 EVs were projected for each of Warwick and Leamington Spa, and in fact 15,000 were to be bought in Warwick and 5,000 in Leamington, the grid would be totally disrupted and unable to cope: our forecasts are too inaccurate (numbers of EVs in 2018 are over 40 times the forecast 10 years before, if I remember correctly), so we must build excess capacity because of the lead time to construct grid reinforcements.

- As the ENA (Electricity Networks Association) will tell you, there is a case study in Southern Australia where investment was deferred as being too expensive; when the need became critical just a couple of years later, it cost three times as much to undertake the work as an emergency programme – so even if a small proportion of the built-ahead-of-need assets prove unneeded, the overall programme cost is greatly decreased by building ahead of need.

- The time and cost to build and install new grid connections is so great that many useful and excellent projects are not proposed: it is not only the direct costs, but the indirect costs of tying up money and resources for extended periods.

- There is a regulatory and governmental obsession that National Grid “gold-plated” the system, but in fact almost every asset built then has proved useful even if that use has come a few years later than the original forecast.

- If we had only built to proven need, the National Grid would never have been built.

- The short-sighted focus on meeting 2030 targets is failing to put in the investment and incentives required to develop, test and roll out the technologies required to meet our 2040 and 2050 targets.

Instead, the government and all regulators and departments should determine their 2050 objectives, together with alternatives, and undertake / incentivise all investments into plant, networks and technologies accordingly. They should structure all contracts and regulations to deliver this. Otherwise the costs of the energy transition will become unacceptably high to the entire country, and be passed onto either government as subsidies or consumers as charges – or both.

The Opportunity

The UK has immense innovative capacity in all fields, including in technologies that lead to decarbonisation. If we overcome the many disincentives in HM Treasury and elsewhere to their development, commercialisation and adoption, the opportunity to develop world-beating businesses, technologies, products and services, and to keep those businesses based in Britain.

This would have the additional benefit of regional re-balancing: most of the industries considered “low risk” by the financial services sector are in the South East; most technical innovation is done and wishes to be developed elsewhere in Britain.

Conclusion

In conclusion, to support the UK economy as a whole and decarbonisation in particular,

- Reduce incentives where there is no technical risk, using this freed-up money to increase incentives for first-of-a-kind plants and products, and their commercialisation;

- Incentivise financial funds to invest at least 5% in technically risky ventures;

- Ensure that strategies, regulations, concepts and incentives are geared towards 2050 targets rather than any intermediate stages;

- Invest in infrastructure according to forecast rather than need, to enable the transition and minimise the cost and timescale of building the infrastructure;

- Re-define energy storage as storage, a grid service, regardless as to whether or not other branches of government do so.

Appendix 5 Regulatory Definition of Storage

What Is Storage?

Storage stores electricity. It does not generate new electricity (except for traditional CAES, see next paragraph): it only re-sells the electricity (minus losses) that it purchased. It is therefore not generation. It moves electricity in time, much as interconnectors move it in location.

Traditional CAES alone is a mix of generation and storage, because it burns fuel to re-heat the air. It can be treated partly as storage and partly as generation, in proportion to the percentage of the output energy that derives from the fuel. Adiabatic CAES does not have this issue: it is pure storage.

Triple Charging

There is a general mis-perception that storage is double-charged for grid access charges: paying for consumption and again for generation. It does, but also the electricity purchased has also already paid charges, so storage is actually triple-charged.

Interconnectors do not pay for grid access, though the electricity they carry has already had grid access charges paid. This is correct: they are merely an extension of the grid, providing grid services. The same is true of storage: it merely provides grid services and therefore should not be charged for grid access.

How the Decision Was Made

Naturally the incumbent generators want to keep it this way, to keep the playing-field tilted sharply in their favour. Storage companies want “zero charging” (i.e. reduce to charging only for the purchased electricity) on the grounds that storage doesn’t generate. So Ofgem decided to split the difference and define storage as generation.

They stated that this was a partial solution, adopted because it didn’t need primary legislation; when the opportunity for primary legislation would occur, then they would seek to create a true definition of storage. However now they are proposing to

define storage in primary legislation, which defeats the purpose of the interim solution and prevents a correct definition.

They now say that they wish to define it as storage because they can base the definition on existing regulatory categories. But that would be the case equally if they based the definition of storage on that of interconnectors – and with fewer modifications needed.

I am told that the industry is happy with the current proposal. Given that the industry is dominated by incumbent generators, that does not surprise me. However the need for change was also identified by the National Infrastructure Commission.

Problems with Defining Storage as Generation

There are many problems with defining storage as generation, which can be summarised as:

Charging

- Grid Code Requirements

- Grid Operator Constraints

- Grid Connection Costs

Contractual

- HM Treasury

- Sundry Regulations

1. Charging

As cited at the beginning of this document, storage is triple-charged for grid access; the proposal is to move it to double-charged. This keeps the playing-field tilted in favour of generation and interconnectors, which are both single-charged – generation as generation and interconnectors within the price of electricity purchased. This therefore subsidises generation at the cost of the bill-payer. It provides even more subsidies to foreign generation and of the UK bill-payer, as grid connection charges for generation are lower on the continent than in the UK and the UK does not charge differential fees (i.e. the difference). It is the bill-payer who loses out most because it disadvantages the most cost-effective means of balancing the grid.

2. Grid Code Requirements

The grid code for generation is loaded with requirements that are suitable for generation (e.g. 15% over-generation capability) but unsuitable for storage. This is right and proper owing to the nature of the generation asset being regulated – but therefore not right or proper for storage. The code for interconnectors does not have most of these, and therefore is much more suitable for storage.

Ofgem says that the grid code is determined by the industry, and therefore the grid code consequences of the regulatory mis-definition of storage are not their responsibility. But this overlooks that (a) the grid code is built on the regulatory definitions and reflects them, and (b) those with the greatest input into grid code matters are the large incumbent generators who have sufficient resources and who also have little interest in storage in comparison with their interest in generation.

3. Grid Operator Constraints

Both transmission and distribution operators are banned from owning generation, with a derogation of up to 6MW for DNOs. Yet both see huge potential benefits from storage, in balancing the grid, in providing stabilisation services, and in alleviating constraints and deferring capital investment. Both would invest in storage if permitted. And both would wish to support storage with NIC / NIA funding, which they are not permitted to do while storage is defined as generation.

Defining storage as storage would enable this. But it would also give the flexibility of allowing, disallowing and/or constraining such ownership and/or operation, as regulations (rather than primary legislation) can be used to do so – if storage is defined as storage rather than as generation.

And the ability to invest NIA / NIC funds in storage and in the issues relating to it (e.g. developing a standard system for calculating its effects on grid capacity, such as alleviating congestion like the Leighton Buzzard and Orkney plants) would greatly assist the network to adjust to a zero-carbon future.

4. Grid Connection Costs

Currently the effects of a proposed plant on grid loads is to calculate its operation as consumption, and again to calculate it as generation. This maximises the cost and lead time of grid connections, thereby making storage much more expensive and severely constraining the locations in which it can cost-effectively be built.

Storage mostly acts counter-cyclically, alleviating rather than creating grid congestion. It is on this basis that the batteries in Leighton Buzzard, Orkney and Eigha were proposed. Therefore grid connection requirements should be calculated based on storage being storage, not on it being generation and/or consumption. Doing so would reduce connection costs and lead times, consequently increasing its roll-out and reducing consumer costs.

Likewise, operational grid access charges would need their own computation to encourage storage to alleviate grid challenges, and thereby speed roll-out and reduce consumers’ bills.

Creating such models would be ideal subjects for NIA / NIC projects. There may be a conclusion whereby different constraints in operating modes of storage would incur different connection construction costs and ongoing charges.

5. Contractual

National Grid is unable to enter into a contract for “storage services” which cuts across many current and proposed contract types, because storage is not legally defined as such. This means that storage has to bid for a huge revenue stack of separate services, every 2 years or less, with many adverse consequences, including:

- The TSO / DSO has huge administrative and grid control burdens as they can’t just ask the storage to respond to a situation – they have to select from a vast menu of situations and responses before triggering each one individually.

- We are eligible for a stack of 12 contracts, with another 4-6 being mooted at present. This means that we have to administer 12-18 contracts concurrently, ensuring correct compliance, invoicing and contract management for each, adding enormously to our administrative costs which we would have to reflect in our prices, which ultimately will cost the consumer a lot.

- Each of these revenue streams needs to be re-bid every 6-24 months, with consequent administrative burden on both us and the TSO / DSO, again adding to consumer costs.

- Each of these bids has a chance of failing to win a contract, meaning that –

- We have to price in the possibility of failure, having to operate for a period without a contract or having to fill that “slot” with a lesser-paying contract;

- We also have to price in the additional administrative costs of having to bid for more contracts than we win;

- Our financing costs will be higher owing to the commercial risk;

- And all these costs will ultimately be passed on to the consumer.

With a regulatory definition of storage as storage, the TSO / DSO would be able to let contracts for “storage services”, maybe split into primary and secondary to reflect different storage types and characteristics – PHES and CAES as primary and batteries / DSR as secondary, with flow batteries maybe being able to choose.

6. HM Treasury

The Treasury offers certain incentives for investment, such as the Enterprise Investment Scheme (EIS), which explicitly list generation as ineligible. The Treasury uses the regulatory definition of storage (currently generation plus consumption) as its own definition. Therefore defining storage as generation will greatly reduce investment into storage, and increase the returns that investors require for doing so, and thereby increase the cost of de-carbonising the grid.

7. Sundry Regulations

Other regulations, such as planning regulations, also base some of their rules on whether or not a plant is or will be generation. Mis-defining storage as generation would continue to ensure that storage is judged by characteristics that it does not possess, often to its (and thus the grid’s and consequently the consumer’s) disadvantage.

Proposal

Define storage, in primary legislation, as storage.

Base the definition on that of interconnectors.

The grid code would therefore be modified, based on interconnectors rather than trying to fit a round storage peg into a square generation hole.

Enable contracts for “storage services” to be let by the TSO and DSOs.

Appendix 6: Scale of the Problem – TINA

Another analysis of the problem, the Technology Innovation Needs Analysis by the Low Carbon Innovation Co-ordinating Group (LCICG), which is the biggest inter-departmental group in the British Government’s civil service, identifies that Britain requires 27.4GW of storage (in the range of 7.2 to 59.2GW), with a capacity of

128GWh (31 to 286GWh). This is 5 hours’ storage at rated capacity, coinciding with the duration of the winter evening peak: almost no grid-connected battery in the world has more than 2 hours’ storage because it is not cost-effective.

This analysis only looks at supporting the country’s currently forecast variable demand, assuming that baseload demand will continue to be supplied by nuclear and gas plants. Therefore if nuclear is to fail to materialise in sufficient volume (which looks increasingly likely), and we cannot increase the gas generation lest we exceed our treaty obligations on emissions, this storage requirement must be increased greatly to accommodate baseload generation.

Even taking the 27.4GW figure at face value and looking at cost-effective developments only, we can expect it to be made up of (additional to what was in place at the publication of the report) 2-3GW (2-3GWh) demand side response, 2-3GW (2-3GWh) batteries, 8-12GW interconnectors and 2GW (20GWh) total of all existing pumped hydro planning applications. This totals 12-18GW (24-26GWh), leaving an unmet need for 7.4-13.4GW (102-104GWh) which Storelectric can supply more cheaply than gas-fired peaking plants.